Canada processed more than 20.5 billion transactions worth $11.7 trillion CAD in 2022 — a market that has expanded every year since. For any merchant entering or scaling in Canada, payment methods in Canada determine checkout conversion directly. This overview maps the full spectrum of options, from dominant card networks to the open banking infrastructure reshaping the market in 2026 and beyond.

How Canadians Pay: Key Market Data

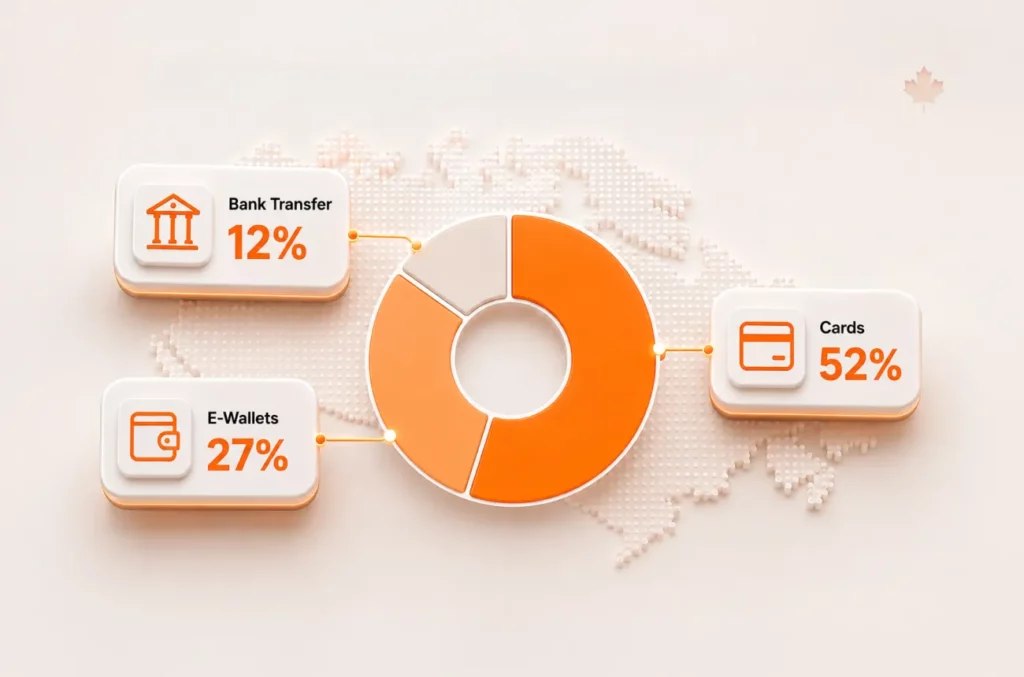

The Canadian payment mix concentrates around three categories, each serving a distinct role in the checkout flow. Cards lead by volume, digital wallets accelerate year-over-year, and bank transfers command a rising share of e-commerce value. Understanding that split prevents costly gaps in checkout coverage.

| Payment Method | Market Share | Best For |

| Cards (Visa, Mastercard, Amex) | 52% | Cross-border, high-value transactions |

| E-Wallets (Apple Pay, Google Pay, PayPal) | 27% | Mobile-first, Gen Z buyers |

| Bank Transfer (Interac, pay by bank) | 12% | Domestic, low-cost, instant settlement |

These three categories cover over 90% of Canadian transactions, making simultaneous support for all three the baseline for competitive checkout.

Interac: Canada’s Native Payment Network

Interac functions as Canada’s national account-to-account payment infrastructure, processing 6.5 billion debit transactions and 1.16 billion e-Transfers in 2023 alone. No other domestic network matches its penetration: half of all Canadian businesses now accept Interac e-Transfer, and the brand carries the highest consumer trust of any payment method in the country.

Three distinct Interac services cover different transaction contexts:

- Interac Debit — point-of-sale card payments, also available through Apple Pay and Google Pay for contactless in-store checkout

- Interac e-Transfer — peer-to-peer and B2C transfers via email or phone number, with Autodeposit enabling fully automated receipt

- Interac Direct (powered by KONEK) — Canada’s emerging account-to-account online checkout solution, replacing the discontinued Interac Online with real-time bank authentication at checkout

Merchants who integrate all three Interac touchpoints eliminate the primary reason Canadian shoppers abandon carts: the absence of a familiar, trusted local payment option.

Cards and Mobile Wallets in Canadian Checkout

Cards account for over 64% of consumer payments in Canada, anchored by Visa at 58% of card market share and Mastercard at 38%. American Express serves the premium segment. Mobile wallets — led by Apple Pay and Google Pay — now power over 37% of payments as of early 2026, growing fastest among Gen Z, where 69% of users reported mobile wallet usage in early 2025.

Credit and Debit Cards: Costs and Tradeoffs

Card processing averages 2.65% per transaction across Canadian merchants, with cross-border and foreign currency fees adding further cost. Chargebacks represent the primary risk layer for card-accepting businesses. That said, cards remain non-negotiable for international buyers and high-value purchases where credit availability drives conversion.

Four structural facts shape card strategy for Canadian merchants:

- Visa dominates at 58% of card transactions — Visa acceptance is the single highest-impact card decision

- Contactless penetration ranks among the world’s highest; the average Canadian adult carries three contactless-enabled cards

- Apple Pay transactions above C$100 process via device verification, removing the standard contactless limit

- 3D Secure (3DS) authentication significantly reduces card-not-present fraud for online merchants

Balancing card acceptance with lower-cost alternatives — particularly for domestic buyers — delivers the optimal blend of conversion rate and margin protection.

BNPL and Emerging Payment Options in Canada

Buy now, pay later services account for approximately 6% of Canadian e-commerce transactions, with Klarna, Afterpay, and Affirm leading adoption. BNPL raises average order values and converts hesitant buyers in high-ticket categories — merchants who offer it alongside standard card and bank-transfer options capture the broadest possible demand without restricting choice.

Four additional payment categories round out the Canadian market:

- BNPL (Klarna, Afterpay, Affirm) — instalment checkout that lifts average order value; merchant fees run higher than card processing, making it a complementary rather than primary option

- Prepaid cards and vouchers — serve unbanked consumers and privacy-focused buyers; strong in iGaming and digital goods verticals

- Cryptocurrency — Bitcoin and select stablecoins accepted by a growing niche of Canadian merchants; adoption remains below 5% but accelerates in tech-forward sectors

- QR code payments — expanding in food service and small retail; direct bank-account debit via scan reduces terminal infrastructure requirements

Each method targets a distinct buyer segment. Merchants who map payment options to customer demographics convert more of their addressable market.

Open Banking Payments: Canada’s Next Payment Shift

Canada’s open banking framework entered active rollout in 2026, following extensive pilot programs throughout 2025. Nearly half of Canadians already recognise the benefits — faster authorisation, lower fees, and real-time settlement — and the infrastructure is now live for early adopters. Merchants who integrate open banking payments now capture first-mover conversion advantage as the Real-Time Rail scales nationally.

Account-to-account open banking payments deliver four structural advantages over card-based checkout:

- Real-time settlement — funds reach the merchant account at the moment of transaction, eliminating the 1–3 day card processing delay

- Lower transaction costs — removing card network interchange reduces per-transaction fees to a fraction of standard card rates

- No chargebacks — the good funds model confirms payment at source; once authorised, transactions cannot be reversed by a buyer dispute

- Reduced fraud exposure — bank-level authentication replaces card credentials, closing the primary vector for card-not-present fraud

Pay by bank via open banking rails positions merchants ahead of the regulatory curve and aligns with the direction Canada’s payment infrastructure is definitively taking.

Start Accepting Open Banking Payments with TODA Pay

TODA Pay delivers open banking infrastructure built specifically for the Canadian market, enabling merchants to accept account-to-account payments through a single API integration — aligned with the 2026 framework now entering active deployment. Access Open Banking Payment via TODA Pay and connect to Canada’s real-time payment rails today.

Frequently Asked Questions About Canadian Payment Methods

What is the most popular payment method in Canada?

Cards dominate Canadian payments, accounting for over 64% of all consumer transactions nationwide. Interac e-Transfer leads account-to-account payments, processing more than 1.16 billion transfers in 2023 alone.

Is Interac the same as e-Transfer?

Interac is Canada’s national payment network, while e-Transfer is one service within that network. Interac also operates Interac Debit for point-of-sale purchases and Interac Direct for account-to-account online checkout.

What payment methods do Canadian online shoppers prefer?

Canadian online shoppers primarily use credit cards, Interac e-Transfer, and digital wallets like Apple Pay and Google Pay. BNPL services from Klarna and Afterpay attract younger demographics seeking flexible instalment options.

Is open banking available in Canada right now?

Canada’s open banking framework entered active rollout in 2026, following a full preparatory phase completed in 2025. Early adopters already access real-time account-to-account payment rails, with nationwide availability scaling throughout the year.

What is the cheapest payment method for Canadian businesses?

Account-to-account transfers via Interac or open banking rails deliver the lowest per-transaction cost, removing card network interchange fees entirely. Pay-by-bank solutions reduce processing expenses significantly compared to standard card rates of 2.65%.